Writing recently in Slate, John Dickerson argues:

"The most likely beneficiary of Warner's departure may be Bayh, who was competing for a similar sphere of donors and activists as a representative of the centrist wing of the Democratic Party. As a former governor of Indiana, Bayh can claim executive experience, just as Warner could, and offer the same hope that as a favorite son he could turn a red state into one the Democrats could count on."

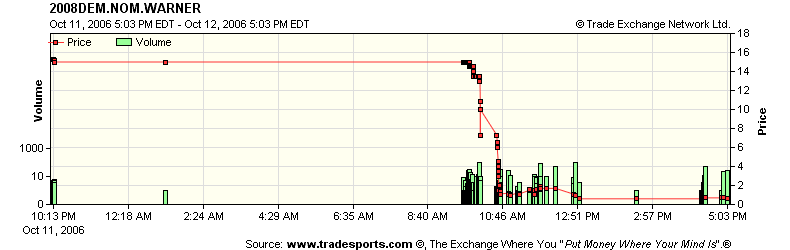

As I noted yesterday, the initial market response to the Warner withdrawal was that Edwards would be the main beneficiary. But there's also some support for Dickerson's view. At around the same time as the price of the Warner contract was collapsing, the price of the Bayh contract jumped upwards:

Still, the rise in price here is small compared to the rise in the Edwards contract, and even the Clinton contract has gone up by more. It'll be interesting to see what happens over the next few days.

"The most likely beneficiary of Warner's departure may be Bayh, who was competing for a similar sphere of donors and activists as a representative of the centrist wing of the Democratic Party. As a former governor of Indiana, Bayh can claim executive experience, just as Warner could, and offer the same hope that as a favorite son he could turn a red state into one the Democrats could count on."

As I noted yesterday, the initial market response to the Warner withdrawal was that Edwards would be the main beneficiary. But there's also some support for Dickerson's view. At around the same time as the price of the Warner contract was collapsing, the price of the Bayh contract jumped upwards:

Still, the rise in price here is small compared to the rise in the Edwards contract, and even the Clinton contract has gone up by more. It'll be interesting to see what happens over the next few days.