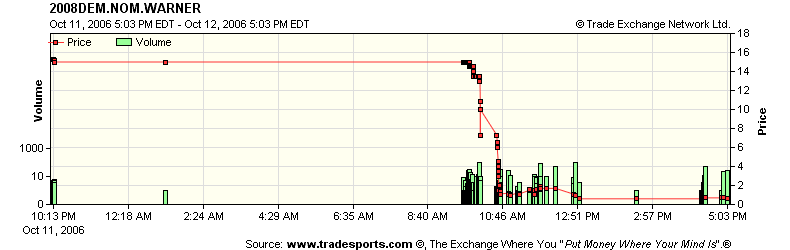

How exactly does new information get transmitted into the prices of financial assets once it becomes publicly available? To me this is one of the most interesting questions in the economics of finance. Sometimes the information has rather obvious price implications. For example, once Mark Warner announced that he would not be seeking the Democratic presidential nomination, the price of the contract 2008DEM.NOM.WARNER (which pays $10 if he is the eventual nominee) dropped rapidly from about $1.50 to practically zero, and has remained there since. It's perfectly obvious to everyone that this contract is very unlikely to pay anything at all.

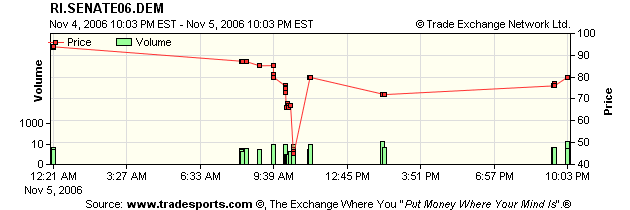

Most of the time, however, new information is much harder to interpret. Today, for example, a new Mason-Dixon poll was released showing Lincoln Chafee up a point in the Rhode Island Senate race, the first time he has led in any poll since August. In fact, the two previous polls in the RCP list had him down by double digits. Clearly, the race there is tightening, and one would expect to see this reflected in the prices of the RI.SENATE06.DEM and RI.SENATE06.GOP contracts. But by how much should the prices change? In other words, to what extent should the new poll cause us to revise our beliefs concerning the likelihood of a Chafee victory?

Well, here's what actually happened to the price of RI.SENATE06.DEM (which pays $10 in the event of a Chafee loss to Whitehouse). The last trade before the new poll became public was at $9.39. Soon after the poll became public on the morning of November 5, the price dropped to $8.73. This was at 8:17 AM. By 9:38 the price was down to $8.00, by 10:08 to $7.50, by 10:22 to $6.70, and by 10:30 to $4.50. By 11:11 it was back up to $7.97, and has remained between $7.00 and $8:00 ever since:

The point is that nobody really knows what the "true" likelihood of a Chafee victory really is, and how exactly to adjust one's beliefs in the face of new information. The market aggregates the opinions of all participants, but does so in a noisy way that can sometimes involve a lot of volatility and overshooting. More interestingly, the process may be path-dependent, since trading alters the distribution of assets and cash holdings among participants, and hence the extent to which their individual beliefs are reflected in the eventual price.